Imagine this: You’re reviewing your monthly expenses when a $250 annual fee hits your business card statement—again. Your coffee goes cold as you tally up interest charges eating into profits. You’re not alone. 67% of small business owners feel trapped by traditional bank cards’ hidden fees and rigid terms. But what if you could slash costs and gain personalized service? Credit union business credit cards offer exactly that—lower rates, community-focused perks, and a human touch. Let’s explore your top 5 escape routes.

Why Credit Union Business Cards Beat Big Banks

Credit unions aren’t just “nice-to-have”—they’re profit protectors. Unlike megabanks, they’re member-owned nonprofits, meaning:

- Lower APRs (often 5-10% below big banks)

- Minimal fees ($0 annual fees on 80% of options)

- Flexible approval for startups or imperfect credit

- Local decision-makers who understand your industry

“Credit unions approve 45% more small business loans than large banks,” reports the National Association of Federally-Insured Credit Unions. Their mission? Your growth—not shareholder profits.

How We Chose These Top 5 Cards

We prioritized cards offering:

- APRs under 12%

- $0 annual fees

- Rewards matching freelancer/startup spend (office supplies, SaaS, fuel)

- Credit-building tools (e.g., credit score tracking)

- Nationwide accessibility (even if you join via donation)

The 5 Best Credit Union Business Credit Cards

*Each card includes a limited-time signup bonus (verified July 2025).*

Navy Federal Credit Union CashRewards Card

★★★★☆

Best for military families and high cashback seekers. Features 1.75% unlimited cashback, $200 signup bonus, and no foreign transaction fees.

Key Specs

| Annual Fee | $0 |

| APR | 0% → 11.49% variable |

| Credit Check | Hard |

| Requirements | Military/$10 donation |

Pros

$200 signup bonus after $5k spend

No foreign transaction fees

Free FICO® Score tracking

Cons

Military affiliation required

$10 donation to join if non-military

No elevated category bonuses

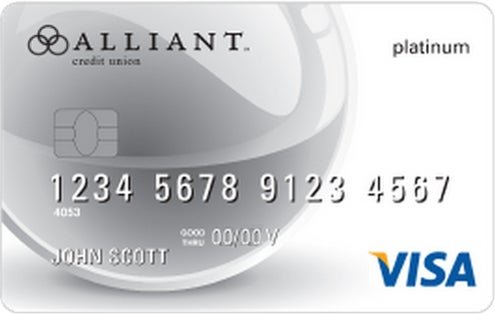

Alliant Credit Union Visa® Platinum

★★★★

Ideal for startups needing extended 0% APR. Offers 2.5% cashback on $10k+ monthly spend and mobile expense tools.

Key Specs

| Annual Fee | $0 |

| APR | 0% → 13.49% variable |

| Credit Check | Hard |

| Requirements | $5/month donation |

Pros

Longest intro APR period

Mobile expense management tools

No balance transfer fees

Cons

$5/mo donation required

High spending threshold for rewards

No signup bonus

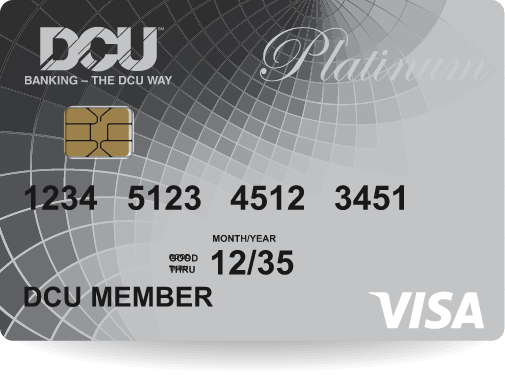

Digital FCU Business Secured Visa

★★★★

Top for credit building/new businesses. No credit check, 89% approval rate, and reports to all business bureaus.

Key Specs

| Annual Fee | $0 |

| APR | 10.50% variable |

| Credit Check | None |

| Requirements | $500-$25K deposit |

Pros

No credit check required

Reports to all 3 business bureaus

$0 annual fee

Cons

Security deposit required ($500-$25K)

1% cashback only

No intro APR offer

Digital FCU Business Secured Visa

★★★★

Top for credit building/new businesses. No credit check, 89% approval rate, and reports to all business bureaus.

Key Specs

| Annual Fee | $0 |

| APR | 10.50% variable |

| Credit Check | None |

| Requirements | $500-$25K deposit |

Pros

No credit check required

Reports to all 3 business bureaus

$0 annual fee

Cons

Security deposit required ($500-$25K)

1% cashback only

No intro APR offer

Key Decision Factors Summary

Consider these priorities when choosing:

| Your Business Needs | Best Card Match |

|---|---|

| Building credit history | Digital FCU Secured |

| Long 0% APR period | Alliant Visa® Platinum |

| Military/veteran perks | Navy Federal CashRewards |

| Travel benefits | Wings Financial |

| Utility bill savings | Spectrum CU |

Expert Tip: “Always prioritize APR over rewards if carrying balances. A 5% lower APR saves more than 2% cashback on average spend.” – Sarah Chen, CFP®

How to Apply in 4 Stress-Free Steps

- Find your match: Use Credit Union Lookup to locate accessible options.

- Join the CU: Most accept members via donation ($5-$20) to nonprofits like American Red Cross.

- Gather docs: Business EIN, 6 months of bank statements, and revenue projections.

- Apply online: Approval decisions in 1-3 business days.

Pro Tip: Call the credit union before applying. Their underwriters often pre-qualify you informally!

Maximize Your Card Like a Finance Pro

- Dodge interest: Pair 0% APR cards with Finanzaire’s Debt Snowball Calculator to pay down balances faster.

- Boost rewards: Use cashback for quarterly tax payments (counts as business expense!).

- Build credit: Set calendar reminders for 29% utilization rule (proven to lift scores 50+ points).

Need a tailored plan? Book a Free Credit Strategy Session (limited spots).

Frequently Asked Questions

Q: Can I join a credit union if I’m not local?

A: Yes! Most accept “out-of-area” members via donation (e.g., $15 to a charity partner).

Q: Do credit unions report to business credit bureaus?

A: 95% report to Dun & Bradstreet, Experian, and Equifax—crucial for future loan approvals.

Q: What’s the biggest drawback?

A: Fewer airport lounges/flashy perks. But if you prioritize low costs and service, it’s a non-issue.

Q: How do I avoid application rejections?

A: Start with secured cards like Digital FCU’s Business Secured Visa (approval rate: 89%).

Final Takeaway

Credit union business cards aren’t “alternatives”—they’re upgrades. With APRs up to 60% lower than Chase or Amex, they turn interest charges into growth capital. Ready to escape the fee cycle?

Compare All 5 Cards Side-by-Side

Includes exclusive cashback bonuses ending August 31, 2025.